by John Weeks

Peddling Ideology as Science

All social sciences carry a heavy burden of ideology, but none heavier or more explicit than what currently passes for mainstream economics. Critics often complain that economists arrogantly pretend to understand far more than they actually do. As I explain in my new book, Economics of the 1%, this criticism is too weak. The mainstream of the economics profession, “neoclassical economics”, claims profound knowledge, yet provides understanding of almost nothing and obscures almost everything by peddling ideology in the guise of analysis. The profession practices and promotes pseudo-science.

Imagine if you can that astrologers seized the observatories, alchemists occupy the chemistry laboratories and creationists dominate the study of genetics. This has occurred in economics, burdening the professional with a dead weight of absurd inconsistencies presented as theory. There is no policy or economic outcome so reactionary or outrageously anti-social that some mainstream economist will not defend it, many will give their tacit support, and very few will denounce it as the ideology it is. Among these reactionary absurdities we find the conclusions that income discrimination by gender and race is an illusion, unemployment is voluntary, and sweatshops are good. I designate this reactionary mainstream to consist of econfakers, practicing a pseudo-scientific fakeconomics, just as astrologers practice astrology and alchemists alchemy.

If after appropriating the profession, the neoclassical school had driven it into disrepute, which would happen if the creationists took over the field of genetics, astrologers astronomy and alchemists chemistry, their offense would rank as a minor intellectual crime. Fakeconomics would wither under ridicule. But to the contrary, the econfakers have successfully sold their nonsense as an unchallengeable wisdom to guide governments. It is not wisdom. On the contrary, it is nonsense, a virus of the intellect.

It is obvious that the nonsense posing as economics gained its ideological hegemony because it faithfully serves the interest of the most reactionary elements of capital. Harder to explain is why so many people in so many countries of the world revere economists as gurus. In great part the undeserved credibility of economists results from the systematic fostering of ignorance. Understanding society’s economy is not simple, but no more difficult than understanding the political system sufficiently to vote. People regularly go into voting booths and choose among candidates or reject them all. Most of the same people would profess an economics that leaves them unable to evaluate competing claims about the state of the economy.

An astoundingly high proportion of the adult population regards the economy and economics as something understood only by experts. It is quite extraordinary that when asked, for example, whether fiscal policy should be more expansionary, people frequently begin statements with, “since I am not an economist…”, or “not being an economist…” If asked whether a national health system should be private or public, the same people would not say, “I am not a doctor, so I can’t comment”. Yet, the health system is at least as technically complex as economics.

Somehow the mainstream economics profession has been successful in convincing people, regardless of level of education or political orientation, that economics is a subject so complex and esoteric that the non-expert is excluded from understanding it. If people do venture opinions on economic issues, it is frequently on the basis of breath-taking banalities and clichés inculcated by the econfakers themselves. Common ones are the vacuous, “well, that’s the result of supply and demand working”; the old cliché, “too much money chasing too few goods” causes inflation; or, the meaningless, “governments should not live beyond their means”.

These are the clichés of the ignorant, repeated shamelessly by the media. Even worse, they are repeated by the “experts” the media bring forth to foster our, and their, continued ignorance. Consider, for example, a typical justification of reducing the government budget deficit by cutting social services when unemployment is high: “the government has to consider the reaction of financial markets”. The insight in that banality is equivalent to seeing the terrible photographs of people leaping to their deaths from the World Trade Center Tower on 11 September 2001, and commenting, “Well, that’s the law of gravity for you”.

The Idolatry of Individualism

From tiny acorns great oaks grow. In a case of nonsense imitating nature, from low and banal theory capitalist economics ascends to great ideological heights. With superficial and simplistic propositions the economics mainstream constructs a great and complex ideological edifice from which it issues oracle-like judgments over the affairs of humankind. The reactionary policy parables of the mainstream derive from a short-list of putatively incontestable propositions.

- Desires and preferences are unique to each person.

- On the basis of these desires and preferences people enter into exchanges of their free will, seeking to satisfy themselves through market exchanges with other people.

- These market activities, including the exchange of a person’s capacity to work, are to obtain the income to buy the goods and services dictated by the person’s desires and preferences.

- Many people seeking simultaneously to buy and sell is competition; and this competition ensures that people buy and sell, including their abilities to work, at prices that are socially beneficial.

- Action by any collective or individual authority, private or public, that restricts the potential for people to buy and sell reduces the social benefits generated by markets.

- In the private sector monopolies (sellers) and monopsonies (buyers) reduce welfare. Much more pernicious are the welfare reducing actions of governments, which proclaim good intentions while restricting freedom. These restrictions include all forms of taxation, which reduce people’s incomes, alter market prices of goods and services, and lower the incentive to work below its “natural” level (that is, its market level). Many government expenditures have the same effect, such as unemployment compensation reducing the incentive to work, and subsidies to public schools that distort individual choice among potential providers.

This short list of literally anti-social generalities can be summarised briefly: people have a desire for goods and services beyond their current earning capacity, requiring them to make choices, to allocate their incomes among their wants in the manner that will best fulfil those wants. For all people added together, wants are unlimited and the resources to satisfy them are finite. Economics is the study of the allocation of scarce resources among unlimited wants to maximize individual welfare. Government actions restrict, limit and distort the ability of people to make their choices. Its role should be strictly limited to minimize those restrictions, limits and distortions.

This is the central narrative of mainstream economists, that markets are efficient organizers of economic life. Its origins in eighteenth century individualism could not be more obvious, for it is the doctrine of the Hobbesian “state of nature” ideologically spun as the language of liberty. Winston Churchill famously defended political democracy by arguing that “democracy is the worst form of government except all those other forms that have been tried” (UK House of Commons November 11, 1947). The mainstream economics profession accepts no such ironic minimalism in its defense of markets.

In the ideological myopia of big money and its economic priests, markets are not only more efficient than alternative methods of allocation and distribution, they are the only efficient method. Even more, markets are efficient if and only if they are not regulated in any manner, when they are allowed to operate freely of intervention by non-market forces (i.e., governments). “Controlled” economies (socialist and communist) are by far the worst and regulated markets in capitalist countries almost as bad.

Economic life organized through free markets is not merely the Best, it is the only Good thing. Irrefutable evidence for this assertion is demonstrated in the fact that markets cannot be eliminated even in the most draconian communist state, they can only be “suppressed”. As a result, attempts at regulation of markets, even more the banning of them, does no more than drive them underground (“black markets”), distorting the natural tendency of people to “truck, barter and exchange” (Adam Smith). Human activity is market driven: There Is No Alternative, the TINA principle so commonly found in the public pronouncements of mainstream economists.

The Fundamental Divide

It is rare in the social sciences — perhaps even in the physical sciences — for different analytical frameworks to be totally different. We usually encounter some common ground even in the face of the most basic disagreements. Closely related to common analytical ground is agreement on the empirical tests which would verify or at least grant greater credibility to one framework over another.

In the economics field the fundamental difference between the neoclassicals, on the one hand, and the entirety of the heterodoxy, on the other, can be stated in one sentence. The entire theoretical edifice of neoclassical economics rests on the assumption of full employment of labor. The neoclassical theory of value (prices), keystone in any economic framework, collapses in the absence of full employment. In the neoclassical analysis the value of any commodity or production input reflects its monetary return in the most profitable alternative use to which it could be assigned (the principle of “opportunity cost”). If an economic system has involuntarily idle workers, the opportunity cost of labor is zero.

At issue is nothing less than the definition of economics itself. Let me demonstrate the split by two quotations from the 1930s, the first by Robbins and the second by Keynes where he reveals the epiphany that forced his break with the mainstream:

Economics is the science that studies human behavior as a relationship between ends and scarce means which have alternative uses. — Lionel Robbins, Nature and Significance of Economic Science, 1932.

…[M]y lack of emancipation from preconceived ideas showed itself in…the outstanding fault of that work [Treatise on Money], that I failed to deal thoroughly with the effects of changes in the level of output. – J. M. Keynes, The General Theory of Employment, Interest and Money, 1936.

The Robbins definition, that students find in textbooks to this day, even putatively progressive ones, requires full employment. If workers are unemployed and factories idle, “means” are not scarce. The theoretical necessity for full employment explains why the neoclassicals must purge any hint of Keynes from the profession. Even to entertain the possibility of involuntary unemployment threatens to destroy the entire neoclassical paradigm. No neoclassical conclusion is safe without the full employment assumption, yet it is in continuous conflict with reality.

The greatest economist of the nineteenth century, Karl Marx, was a less-than-full-employment theorist. He shared with Keynes the analytical insight that in a capitalist economy aggregate demand determines aggregate output. Marx pursued the implications of less-than-full-employment more profoundly that Keynes, stressing the driving role of capital, rather than Keynes’ underconsumption approach. But we should not deny the importance of Keynes in attempting to affect the economics equivalent of a Copernican Revolution. In the case of economics, the Ptolemaic disciplines expelled the Copernicans.

The Copernican Revolution in astronomy and the Keynesian Revolution in economics, one victorious, the other defeated by counter-revolution.

What appears as an intellectual division is the ideological manifestation of the fundamental political struggle in almost all advanced capitalist societies, between the tiny minority that controls production and finance, and the vast majority that work for the minority. The full employment framework is non-credible to the point of absurdity and beyond. In no other intellectual discipline would such a chaotic collection of logical inconsistencies and arbitrary assumptions be taken seriously. The full employment paradigm is based on an unambiguously false premise: that the normal condition of capitalist economies is full employment. Yet, this framework dominates mainstream economics, the media and political debate. The less-than-full employment or demand-constrained framework, as obviously sensible as its opposite is absurd, has been relegated to the margins of the discipline.

This inversion, in which the absurd is embraced as science and science is dismissed as absurd, reflects the great victory of the minority over the majority during the final decades of the twentieth century after a brief interruption during the 1950s and 1960s. For almost sixty years, 1870-1930, a relatively primitive form of the full employment framework dominated the emerging economics profession. During the early stages of development of this framework, the undisguised purpose of leading economists was to refute Karl Marx and justify capitalism.

Two great human disasters prompted a rebellion against the free market doctrine, the Great Depression and the Second World War. It was obvious to all that the first resulted from the excesses of a capitalism unconstrained by public regulation. The second was the consequence of the first. Denying this chain of causality requires considerable intellectual invention. By the end of the war a broad consensus emerged in Europe and North America that the excesses of capitalism demanded strict regulation of markets, and especially of the financial sector. This consensus could be found in the most prestigious journal of the profession, the Economic Journal, where K. W. Rothschild asserted that fascism was the fruit of unregulated markets

…[W]hen we enter the field of rivalry between [corporate] giants, the traditional separation of the political from the economic can no longer be maintained. Once we have recognised that the desire for a strong position ranks equally with the desire for immediate maximum profits we must follow this new dual approach to its logical end. Fascism…has been largely brought into power by this very struggle in an attempt of the most powerful oligopolists to strengthen, through political action, their position in the labour market and vis-à-vis their smaller competitors, and finally to strike out in order to change the world market situation in their favour. (Rothschild 1946: 317)

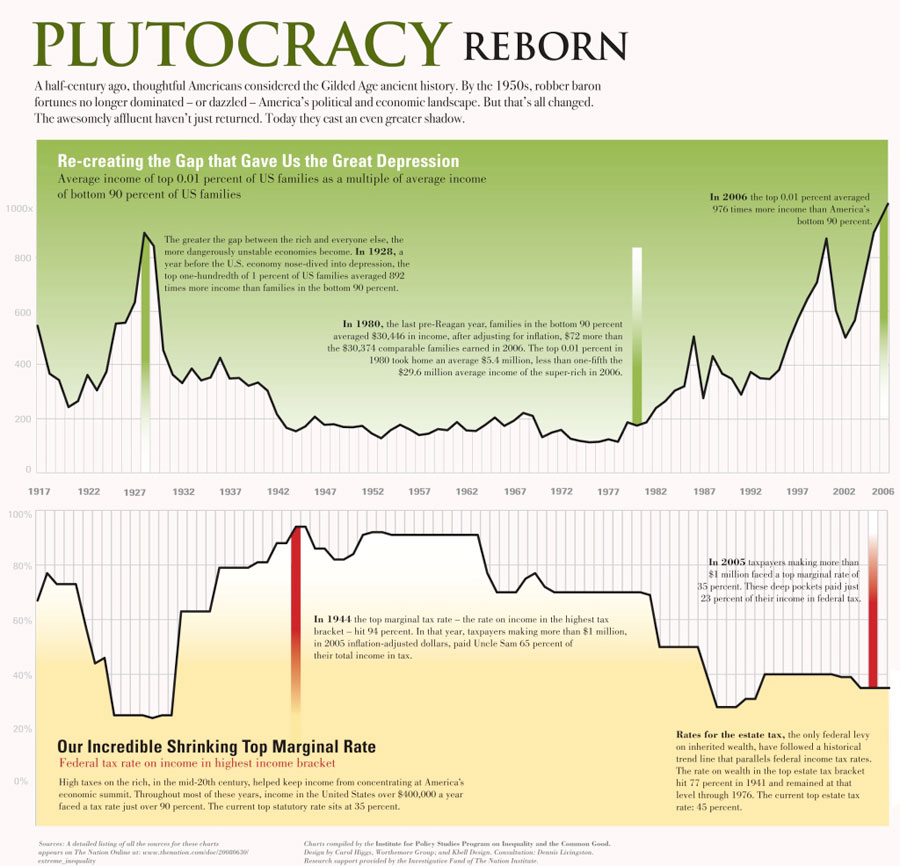

The minority that controlled production and finance considered this consensus a temporary arrangement to be destroyed as soon as possible, because its main economic consequence was to limit the freedom of capital. Those who judged the post-war regulated capitalism as a new norm would be quickly proved wrong. The system of international regulation of exchange rates ended in 1970, deregulation of the financial sector in the United States and parts of Europe began in the 1980s, and the decline of the political base for a managed capitalism, the trade unions, fell into secular decline in most advanced countries. The collapse of the Soviet Union complemented these trends, eliminating the global rival to unmanaged capitalism.

The purpose of destroying the post-war regulatory consensus was to liberate capital from civilizing constraints. The macroeconomics of Keynes and those he influenced provided both the theoretical explanation for why these constraints were needed and the practical policy tools to manage an economy within those constraints. The “Keynesian revolution” briefly institutionalized the singularly sensible principle that governments have policy tools that they can use to pursue the welfare of the populations they were elected to serve. The most important of the tools are fiscal policy, monetary policy and management of the exchange rate. The active use of all these tools was implied by another sensible proposition, the Tinbergen Rule, which states that achieving several policy goals requires an equal number of policy instruments. For example, a government seeking internal and external stability would use fiscal policy to reach a desired unemployment rate, monetary policy to make that unemployment rate consistent with a target inflation rate, and adjust the exchange rate to maintain a sustainable balance of payments.

The obviously sensible proposition that governments should use the tools available to them to pursue the public welfare, while enforcing constraints on the excesses of capitalism, would be discredited by repeated ideological attacks beginning in the 1970s. The constraints would be dismantled and tools de-commissioned by increasingly reactionary governments. Against weak internal opposition the economics profession would provide the ideology for the de-commissioning of the policy tools to support those constraints.

De-commissioning Democracy

The ideology of full employment economics has a clear purpose, to remove economic policy from democratic control. Until the Great Depression of the 1930s, macroeconomic policy in the advanced countries meant monetary policy; exchange rates were tied to an international gold mechanism and fiscal policy constrained by the goal to balance public budgets. Fiscal policy was used by a few governments during the depression, notably in the United States, but in an ad hoc manner. Perhaps the first clear legal commitment to an active fiscal policy was the US Full Employment Act of 1946, the preamble of which states, “The [US] Congress hereby declares that it is the continuing policy and responsibility of the Federal Government to use all practicable means…with the assistance and cooperation of industry, agriculture, labor, and State and local governments…to promote maximum employment, production, and purchasing power”.

In the early 1970s, right wing elements in the economics profession would initiate an assault on this legal commitment, with an analytical de-commissioning of fiscal policy. The right wing of the profession argued, with the logical consistency that frequently accompanies madness, that since the economy was continuously at full employment public policy interventions were unnecessary.

Before Keynes economists argued that the unemployment one observes is voluntary, the result of minimum wages and trade union pressure in labor negotiations. However, the membership and economic strength of trade unions declined after 1970 in advanced countries and problems of enforcement and erosion through inflation made minimum wages a weak reed for a general theory of voluntary unemployment. Unemployment compensation itself, a major reform arising from the Great Depression, offered an alternative explanation. Unemployment persists because payments to the unemployed reduce the incentive to seek work, an argument that would garner a Nobel Prize in Economics in 2010. The argument carries great political power, because it converts involuntary misery into willing avoidance of work, and cautions that well-meaning reforms make matters worse.

The combination of the full employment assumption and benefit-induced unemployment are necessary elements to de-commission fiscal policy. The sufficient argument is that active fiscal measures, even if they were to temporarily reduce unemployment, are intrinsically undesirable. An active fiscal policy is rendered undesirable through three complementary and equally fallacious arguments, all focusing on public sector deficits: direct crowding out of private expenditure, inflationary impact and reduction of private confidence.

First, a fiscal expansion would directly reduce private expenditure (crowding out) and would be realized through a rise in interest rates. Second, the argument that fiscal expansion and fiscal deficits cause inflation is in part designed to rescue the crowding out argument. If all else fails to convince, the agents of capital play their trump card — fiscal deficits reduce private sector confidence. The great strength lies in its vagueness that makes it almost impossible to refute.

One of the few progressive aspects of US economic policy institutions is the legislatively mandated political oversight of the central bank, the Federal Reserve System (FRS). This oversight is through required reports to Congress, which typically involves testimony by the FRS chairman. In addition there is a requirement that the board of governors of the Federal Reserve System has “fair representation of the financial, agricultural, industrial, and commercial interests and geographical divisions of the country”. Perhaps more important, the Federal Reserve System has a mandate that requires it to consider employment as well as inflation — “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates”. In practice the effectiveness of the political oversight has waxed and waned, depending on the chairman and the politics of the time.

In Britain until the Labour Government of 1997 the Bank of England, and therefore monetary policy, was under the direct control of the elected government of the day. Gordon Brown changed this relationship fundamentally, assigning major issues to an unelected “Monetary Policy Committee”. He and others, especially in the City, lauded this change as extracting monetary policy from the whims of politics and placing it into the hands of “experts”.

The so-called independence of central banks, a dogma zealously pursued by the International Monetary Fund, is profoundly anti-democratic. The essence of the argument is that monetary policy is a technical matter, and any degree of democratic oversight results in reckless and irresponsible policies. As for fiscal policy, monetary decisions are not a matter for public involvement. They should be under the dictatorship of a technical elite.

Who Decides Policy?

The reactionary program is especially pernicious because it need not be defended on its intrinsic merits. Its ultimate justification is the infamous TINA principle: there is no alternative. The theoretical conclusion that flexible exchange rates stabilize economies may prove wrong, but would be of no practical consequence because there is no alternative. A balanced public budget may have a pro-cyclical effect on the economy, deepening recessions and exaggerating booms, but deficits would produce worse outcomes. Using monetary policy in the single-minded pursuit of lower inflation may result in persistent unemployment and slow growth, but failing to do so courts disaster. Balanced budgets, low inflation and flexible exchange rates are all necessary to prevent adverse reaction in “financial markets”, discussed in the next section.

The power of these arguments comes from their repetition and the money behind them, not from their theoretical or empirical validity. They are based on a theory that is internally contradictory and ideologically driven. The fundamental issue in a democratic society is not whether inflation, deficits or unemployment are too high or too low. The fundamental issue is — who decides? The general rule in democratic societies is that experts advise and democratically elected representatives decide. Mainstream economics provides the ideological foundation for canceling that rule: elected representatives should enact laws that make the advice of neoclassical experts legally binding. Then, the danger that the many will pressure for policy that limits the privileges of the few is minimized.

There is an alternative to the Hobbesian neoclassical world in which the capitalist minority defines and limits social and economic policy. As happened in the 1930s in the United States, the crisis of the 2000s demonstrated that a range of government actions could be effective to rescue national economies from collapse. The experience of the United States and Western Europe after the Second World War, during the so-called golden age of capitalism, suggests what the component parts of the alternative must be. The reconstruction of a capitalism controlled for the common good will require the reassertion of the strength of trade unions in advanced countries.

Controlling capitalism would require four fundamental reforms, whose purpose would be to severely restrict the economic and political power of capital. First, because capitalist economies do not automatically adjust to full employment, governments must institutionalize an active countercyclical macroeconomic program. The active element in the countercyclical program would be fiscal policy, supported by an accommodating monetary policy, and, if necessary, with exchange rate management and capital controls to stabilize the balance of payments.

Countercyclical policies, and many other sensible and humane economic measures, are dismissed as impractical because of the alleged affect they might have on “financial markets”. This personification of markets, universal in the media and appallingly common in the economics profession, is an essential part of the justification of a capitalist economy free from the constraints of democratic oversight. This personification is applied across all types of markets, as if the market itself were an independent actor in society. In the twenty-first century it became integral to the justification of a socially dysfunctional financial system, national and global.

This personification, an ideological abstraction from the real world of speculators and financial fraud, is an essential part of the mystification of financial behavior. It facilitates the mythology that the dysfunctional financial system is not the work of men and women (mostly the former) within institutions that have socially irrational rules and norms. It promotes the disempowering argument that financial dysfunction is a manifestation of the inexorable operation of the laws of nature that no government can change. It seeks to hide that specific financial speculators wish to coerce governments to take actions in their narrow economic interests.

While it is in the interests of capital to exaggerate the power of finance, the dire warnings about the behavior of financial markets carry some truth. The solution to this threat to humane macroeconomic policies is to tame those markets, not to yield to them. The manner to tame them is public control of the financial sector. In part this could be through direct nationalization, and in part by conversion of financial activities into non-profit or limited profit associations such as mutual societies and savings and loan institutions (building societies). Even in the United States, the heartland of minimalist public regulation, non-profit and limited profit financial institutions have been common in the past.

Third, government regulation of internal markets would be based on the principle of the International Labor Organization that “labor is not a commodity”. The purpose would be to eliminate unemployment as a mechanism of labor discipline. The most effective method to achieve this would be a universal basic income program. A properly designed universal income program would facilitate labor mobility, by reducing the extent to which people were tied to their specific employer. Also, by reducing the volatility of household income, it would provide an automatic stabilizer at the base of the economy, the labor market. It would be similar to the automatic stabilizing effect of unemployment compensation, and more effective.

Fourth, and the basis for all others would be the protection of workers’ right to organize. The program of fundamental reform of capitalism would be based on the political power of the working class, in alliance with elements of the middle classes. This is the political alliance that brought about major reforms throughout Europe after the Second World War. An effective reform of capitalism that eliminates its economic and social outrages requires a democracy of labor and its allies in which the political power of capital is marginalized.

For 250 years a struggle has waxed and waned to restrict, control or eliminate the ills generated by capitalist accumulation: exploitation of labor, class and ethnic repression, international armed conflict, and despoiling of the environment. When a progressive majority has allied, this struggle would have brought great strides. When capitalists, the tiny minority, have been successful in creating their own anti-reform and counter-revolutionary majority much is lost. The last thirty years of the twentieth century and into the twenty-first was such an anti-reform period during which capital achieved a degree of liberation it had not enjoyed for 100 years. With the rise of capital many of the more absurd elements of neoclassical economics, such as the alleged stabilizing effect of financial speculation, manifested themselves in reality, as nature imitated bad art.

The sufferings caused by the Great Depression of the 1930s, quickly followed by the horrors of the Second World War, generated a broad consensus in the developed countries. This consensus agreed on the need for public intervention to protect people against the instability and criminality that results from the accumulation of economic and political power by great corporations. Franklin D. Roosevelt, four times elected president of the United States, had this dangerous power in mind when he addressed the US Congress in 1938:

Unhappy events abroad have retaught us two simple truths about the liberty of a democratic people. The first truth is that the liberty of a democracy is not safe if the people tolerate the growth of private power to a point where it becomes stronger than their democratic State itself. That, in its essence, is fascism — ownership of government by an individual, by a group or by any other controlling private power. The second truth is that the liberty of a democracy is not safe if its business system does not provide employment and produce and distributes goods in such a way as to sustain an acceptable standard of living. Both lessons hit home. Among us today a concentration of private power without equal in history is growing.

The advanced industrial countries, especially the United States and the United Kingdom, reached the point early in the twenty-first century in which private power was stronger than “their democratic state”. This private power manifested itself in unconstrained corporate control that over-rides democratic decisions, justified by an ideology of self-adjusting markets. Rejection of that ideology and fundamental reform of those markets is required to prevent unconstrained corporate power from a latter-day realization of the fascism Roosevelt warned against.

[Thank you indeed John for this contribution.]

The writer is Professor Emeritus, SOAS, University of London, and author of a new book that in non-technical language explains the fallacies of mainstream economics, Economics of the 1%: How mainstream economics serves the rich, obscures reality and distorts policy, Anthem Press. His website is http://jweeks.org

If publishing or re-posting this article kindly use the entire piece, credit the writer and this website: Philosophers for Change, philosophersforchange.org. Thanks for your support.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License.

Excellent analysis by John Weeks. Nationalize the Federal Reserve.

Reblogged this on ΕΝΙΑΙΟ ΜΕΤΩΠΟ ΠΑΙΔΕΙΑΣ.

Excellent article and clear cut exposition by John Weeks, I shall be a fan of your writings henceforth